The next 10 years.....

Some thoughts and reflections.

Hi,

Welcome to Decade of 2020, a newsletter that will relentlessly focus on how the next 10 years will affect the middle class. Forewarned is forearmed, they say. If you’d like to sign up, you can do so here. Or just continue to read…

It is still early days to be able to begin speaking about the path toward recovery after most of humanity received a much needed shock-primer on volatility (i.e rapid change). In a span of 60 short days, Nature reminded the entire human race that the concept of stability is pure fiction.

Volatility alone is permanent, all else transitory. The corona virus taught a few of us to view life through this lens. Some might still crave for the good old stability. I wish them luck.

“Volatility is an instrument of truth.”

Christopher Cole, CIO of Artemis Capital Management

Predicting is dangerous and history is rife with examples of the best having failed at this game. However, taking no risk is taking the greatest of all risks. So here goes my attempt. Firstly, I envisage that in this coming decade we will see much more volatility - in the economy, stock markets, the energy complex, commodities (base and precious metals), in the political sphere, and in society. And YES, we will have a few of those “weeks” that Lenin talked about.

“There are decades where nothing happens; and there are weeks where decades happen.”

Vladimir Ilyich Lenin, Leader of the Soviet Union.

Secondly, the narratives that will compete to shape our perceptions over the next 10 years will mostly be centered around four words:

Deglobalization

Demographics

Debt

Deflation

Deglobalization

I firmly believe that globalization is on its last legs. This may sound contrarian with Apple moving production to India (out of China) but hear me out.

The past twenty years were the final decades of this phenomenon that began in the early 30’s and accelerated in the 60’s. The ascension of China into the World Trade Organization (WTO) circa 2001 marked a definite change in business policies of American multinationals. Laws were soon enacted allowing the likes of GE, 3M and Boeing to open factories and plants in China, and transfer patented technology under stringent agreements; most of which China ended up violating without any fear or apprehension.

The hollowing out of the Rust Belt by virtue of job losses and resulting societal upheaval led to the doors of populism being flung wide open, and an opportunist Trump taking the White House. Once the noise around repealing Obamacare was over, Trump focused on what mattered - China. Protectionist trade policies and tariffs, primarily targeting China, followed. Canada and Mexico weren’t exactly spared either but let’s leave them out of this discussion.

Just before the outbreak of the corona virus, the US China Trade War 1.0 reached its crescendo: the US Senate unanimously passed the Hong Kong Rights and Democracy Act in November of 2019, thus poking China in the eye. Although the political class in the US cannot agree on anything - literally, there is bi-partisan support in waging an intellectual, moral, cultural, currency, trade and, in the future, a kinetic war against China. And the US expects this approach to be embraced by those it likes to call its “allies” in the region - Japan, South Korea, India.

Before the US could talk decoupling openly, Japan said, “Hold my beer!”.

Japan’s PM Shinzo Abe recently called on Japanese multinationals to cut supply chain reliance on China and promised that the government will foot the expenses of moving their manufacturing back home.

“To help them do it, Abe has earmarked about 240 billion yen (S$3.2 billion) to support domestic companies in decoupling their supply chains from China, especially those in high value-added manufacturing.“

Article published in The Strait Times, April 19, 2020.

Some influential voices inside the Washington apparatus are calling for the US to move their pharmaceutical supply chain back to the American soil in the wake of the Corona virus. This, in my opinion, is still the beginning; the election of Trump and Brexit being key early milestones. There is too much turbulence right now for me to effectively separate the wheat from the chaff in order to present actionable thematic investing ideas, but the trend seems to have become clear.

“Volatility is greatest at turning points and diminishes as a trend becomes established.”

George Soros, “The Alchemy of Finance” pg 170.

Demographics

Most of us have read articles written by globalist shills about robots serving delicacies to their patrons in restaurants and cafeterias in Japan. In my opinion, this is not a technological feat per se but more a symptom of a nation in a demographic death spiral (article - ***highly recommended***).

When societies grow wealthy, they tend to forget to have children. The wealth of a nation is, first and foremost, its human capital. This is because all the advancements in science, industry, arts and culture emerge from it.

“Demography is destiny.”

Auguste Comte, French sociologist and father of Positivism

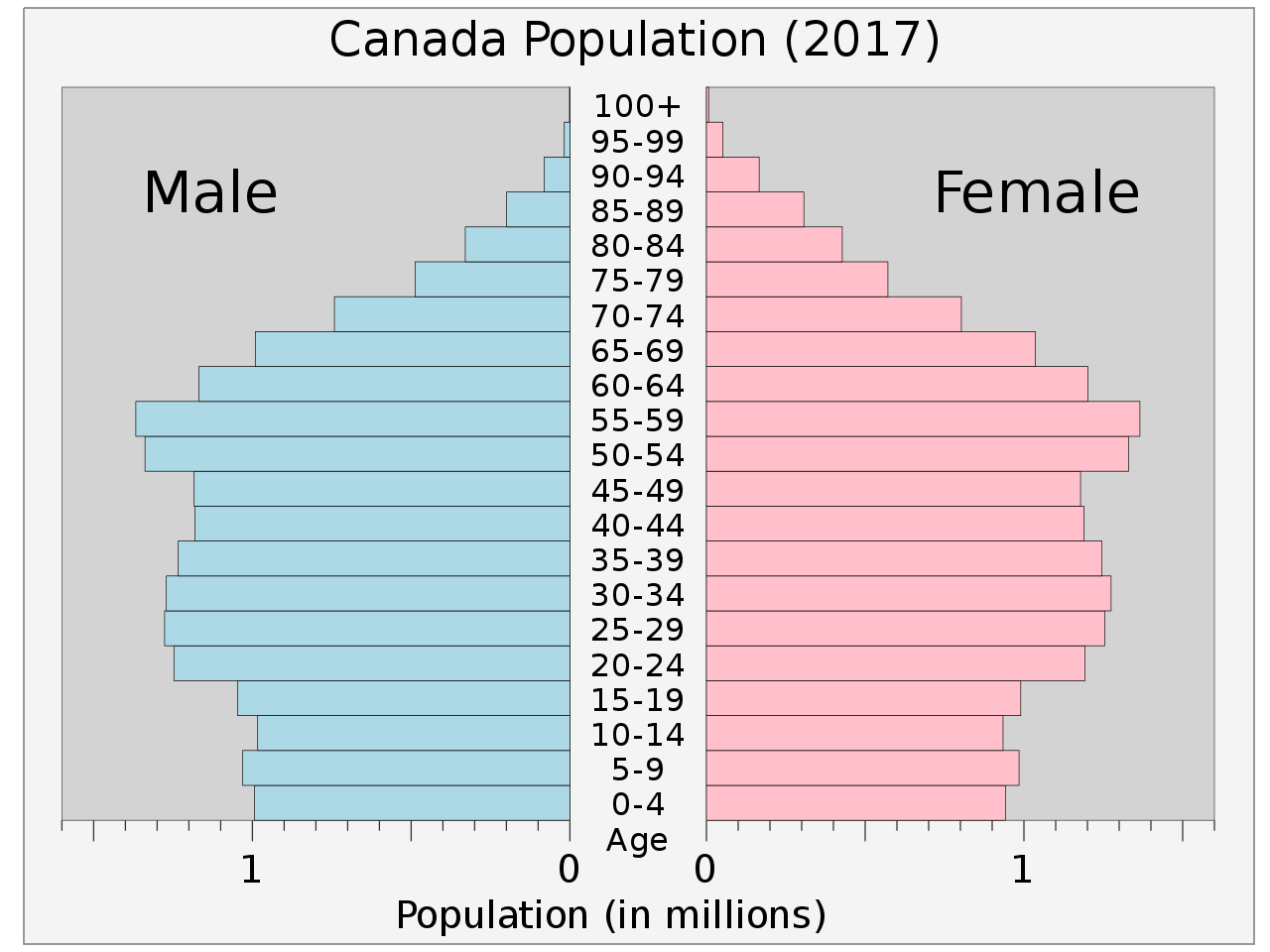

Roughly 35% of Canada’s population is over 55 years. Nearly 40% of the population is in the 25-54 year bracket, which is healthy. What is worrying is that the age bracket that follows this - the 15-24 years category is merely 11% of the overall, as seen in Canada’s population pyramid circa 2017 (below). To put it in context, we have a fast aging population and the “replacement population” is not keeping pace, potentially creating a strong demographic headwind in the coming decade. The story in the US is slightly better but not too different.

The answer obviously, has been immigration. However, it is a sticky and polarizing issue to begin with and most agree it needs to occur in a slow and gradual manner to allow retraining, cultural integration and economic absorption to avoid building a “patchwork nation”.

Debt

To a Canadian, this chart of Private Debt to GDP (expressed as a percentage) must hardly come as a surprise.

The housing market here has long been treated like a casino; the supporting (false) assumption being that property prices always go up. The bubble in housing received validation with the steady flow of immigrants who were keeping demand for the rental market hot since 2011. Those suffering from FOMO joined the herd post 2015, further crowding this trade. Easy availability of HELOCs (Home Equity Line of Credit) coupled with historically low interest rates added gasoline to the blazing inferno.

The wisdom of crowds became the madness of the crowds. Then the corona virus showed up. One of the first reactions of Canada’s banking oligopoly, perversely enough, was to reduce, and in some case completely withdraw, the HELOC lines previously extended to their “esteemed” clients.

Just like many businesses, a sizable percentage of individuals in the US and Canada were carrying an unsustainable debt burden that was pinned heavily to their jobs. Once the pandemic slammed the economy shut and their jobs went away, systemic over-leverage meant savings were non-existent. Finally, with the HELOC lifeline gone, for some, the result was disaster.

“Only when the tide goes out do you discover who's been swimming naked.”

Warren Buffett, at Berkshire Hathaway Investor Conference

Insolvency expert at Hoyes-Michalos and a frequent guest on BNN Bloomberg, Scott Terrio (@ScottTerrioHMA) put it best.

The political cycle here onward may speak of redistribution, and when dressed and marketed in the skin of The Green New Deal, the wolf of Socialism might look like a cute lamb. Especially to the asset-poor Millennial cohort, who are poised to become the dominant voting class in 2022. Just like Universal Basic Income (UBI). Till a few months ago, UBI was perceived to be a horrendous, evil globalist plan of enslavement and there it is being widely implemented right as we speak, in response to the pandemic. But I don’t wish to get too ahead of myself, the spotlight for now must remain on the ongoing debt deleveraging.

Deflation

Many influencers have created an endless stream of Youtube videos and “finance research” with a view to scare-monger the regulars into believing hyperinflation can happen any day in the US - and by extension in all Western economies. Their core argument is correct, their intent not so much. The money printing binge that the Federal Reserve embarked upon as a knee-jerk response to the corona virus might cause a significant dent in the confidence enjoyed by the US Dollar. And America’s hegemony is based on it, plain and simple.

Point taken. But the money that the Fed printed didn’t hit Main Street. Not yet. The proof is hidden in plain sight in the guise of the Velocity of Money data (below). This is the chart the media doesn’t like to talk about because it makes a huge number of their 2000 word articles talking about end-of-times, Weimar style outcome entirely meaningless. I urge you to do more digging into this.

In the aftermath of the 2008 Great Financial Crisis (GFC), the response of the powers-that-be was to legally constitute a form of socialism for the top 10% and a form of brutal Darwinian capitalism for the bottom 90.

And when interest rates were artificially suppressed to ZERO, everything became a commodity - housing, commercial RE, stocks, land, any asset class you can think of, skyrocketed. Those with assets became richer, those without, more desperate. Induced asset inflation worsened their plight, and stagnating wages rubbed salt in the wounds.

However, if you think the governments are going to operate by the same playbook they used in 2008, think again. The very mention of bailing out airlines affected by the corona virus created an angst among the millions already unemployed. The backlash was the cue for some virtue-signaling, power-hungry politicians to come out in throngs to detest share buy-backs by United et al (which were indeed illegal till the late 70’s).

Make no mistake: the amoral political class, greedy Wall Street and the corrupt Hollywood elite benefited by selling us the “Outsourcing will bring efficiency” lie; they will now profit by parroting the “Bring manufacturing back home!” BS. Manufacturing may come back but not the jobs necessarily because of the amazing advances that have been made in autonomous robotics in the last 20 or so years.

As the decade of 2020 progresses, we will see the cantilever supports currently placed by the Western governments under zombie businesses slowly taken away. What will follow is wave after wave of bankruptcies - also called Deflation. And this is how real Capitalism is supposed to work - perform or perish. When a business goes bankrupt, it rarely goes to the graveyard. Debt gets swapped for equity and debt restructuring occurs; this means the interest expense on the balance sheet gets significantly reduced. The business therefore, has a better chance of survival absent activist investors or vulture PE firms, or a toxic combination of both. The overall impact of this kind of widespread debt restructuring is deflationary. But that is not the only outcome:

Deflation also makes the burden of debt heavier, as the same fixed dollar amount of a loan (the "nominal" amount) stays the same, but wages and prices fall……

Article published in Foreign Policy, April 29, 2020.

Don’t get me wrong, we will have high inflation in the West. But only after we endure the short yet painful and visceral deflationary spiral which will likely ruin the over-leveraged portions of the economy. More on that later.

Very nicely written with different views, worth thinking over it..but consistency of Trump govt is questionable..

Well written article relevant to today's needs. Looking forward to more.